Choosing a home insurance company entails locating the best overall combination of low rates, excellent customer service, and coverage options that meet your needs. We gathered thousands of home insurance quotes in order to find the best company for a wide range of Utah homeowners. We discovered that the best price for a typical homeowner in Utah is $425 per year. However, we recommend that you consider more than just which company has the lowest rates.

Home insurance in Utah

When purchasing home insurance for your property, be aware of the coverage options that can be added to the policy for added security and peace of mind. The coverage options you select will most likely be determined by a number of factors, such as the climate in your area, the rate of crime in your area, and the most common causes of property damage.

How much is homeowners insurance in Utah?

In Utah, the average cost of homeowners insurance for a $250,000 dwelling is $647 per year. This is less than the national average of $1,312 per year for homeowners insurance, and it is even less than the average premiums in neighboring states such as California and Colorado.

Related Articles: Easy Own Homes: Rent to Own Homes in Illinois, Missouri

However, keep in mind that home insurance premiums vary depending on the age, size, location, and condition of your home, as well as the coverage options included in the policy. It is also highly recommended that you shop around and request quotes from multiple insurance companies to ensure that you are getting the best rate for your home.

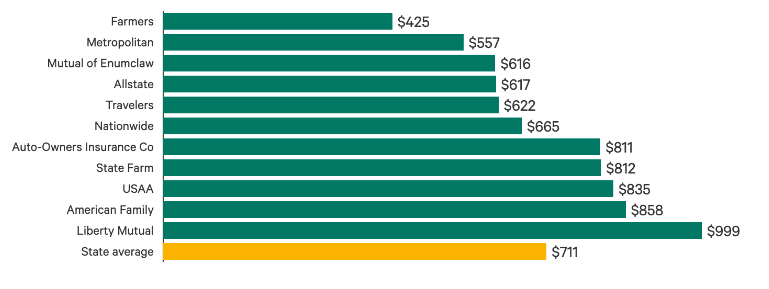

The cheapest options for homeowners insurance in Utah

Home insurance in Utah can cost hundreds of dollars per year, so shop around for the best deal for you. We also gathered thousands of home insurance quotes to determine which insurance company offers the best rates to Utah residents.

Farmers Insurance offers the most affordable home insurance rates in Utah. Our sample property had a typical price of $425, which is an impressive 40% less than the statewide average.

Best Home Insurance Utah

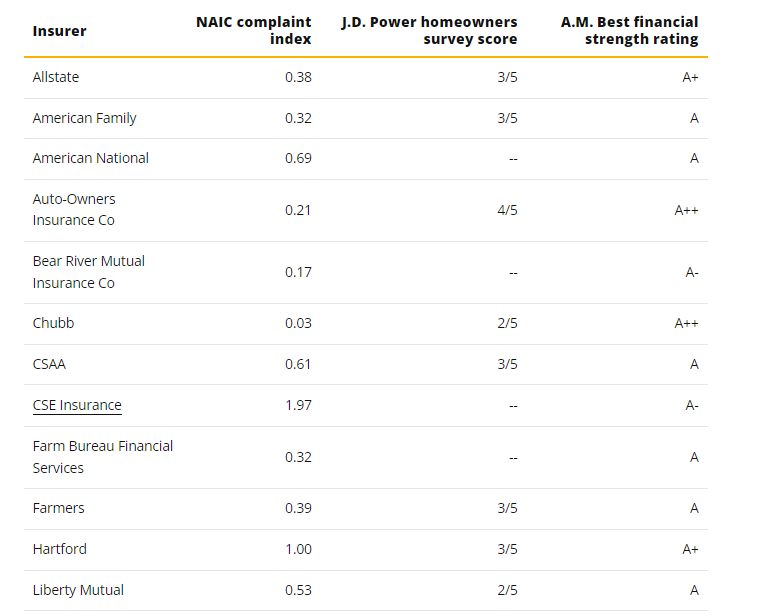

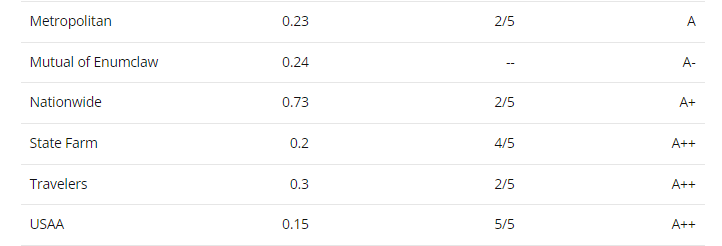

With so many property insurers in Utah, your options for a provider are nearly limitless. Bankrate examined numerous insurance providers in the state to learn their financial strength ratings and customer service scores from reputable third-party reviewers such as AM Best and J.D. Power, as well as each company’s coverage options, discounts, and even mobile app accessibility. Based on our evaluation, the following are some of the best home insurance companies in Utah:

#1. Allstate

Allstate has simple and easy-to-use online tools for first-time buyers, as well as high customer satisfaction ratings. When it comes to average annual premiums, Allstate is one of the most expensive on this list, but they also have a full menu of additional coverage options and discounts that many competitors may not offer to insure your home.

Related Articles: HARLEY INSURANCE: H-Davidson Insurance Policies, Coverages & Discounts (Detailed Review)

More information can be found at Allstate Insurance Review.

#2. Auto-Owners

Auto-Owners collaborates with local agents to guide you through the insurance purchasing process for a more personalized experience. Even when upgrading to its Homeowners Plus policy, its homeowners policy is more standard compared to other homeowners insurance carriers, but the company did receive a high customer satisfaction rating from J.D. Power and a strong financial strength rating from AM Best.

More information can be found at Auto-Owners Insurance Review.

#3. Farmers

Farmers may be at the top of the list for homeowners who have put a significant amount of work into their homes. Though the average home insurance cost with Farmers is slightly higher than the average rate in Utah, the company offers a variety of discounts, specifically for home upgrades and renovations, that may help to lower the premium.

Learn more: Farmers Insurance Review

#4. State Farm

State Farm is a good option for homeowners who want access to a wide range of homeowners insurance policy coverage options, as well as the dependability of a local agent. Furthermore, state farm is on the higher end of the average home insurance premiums on this list, but it also offers a variety of discounts that could help lower the annual premium.

Learn more: State Farm Insurance Review

#5. USAA

USAA has some of the lowest average homeowners insurance premiums in Utah, as well as a variety of coverage options for customization. However, USAA has very strict eligibility requirements and is not available to the public, as the company only accepts honorably discharged current and former military members, as well as eligible family members.

More information can be found at USAA Insurance Review.

Mobile Home Insurance Utah

According to the most recent U.S. Census, Utah, the Beehive State, had 39,267 occupied mobile homes. This type of housing allows many Utah residents to become homeowners at a low cost. Whether you own a traditional trailer-type home or a permanently installed manufactured home, a comprehensive mobile home insurance policy can help protect your investment. If you are one of the 5.1 percent of Utah homeowners who own a manufactured home, comparing manufactured home insurance quotes can also help you save money by ensuring you are getting a good policy at a competitive rate.

Related Articles: West Bend Insurance: Complete Product Review

To find the best insurance plan in your area, use this independent agent matching system. You tell what you want, and the search engine will recommend the best agents for you. Also, any information you provide will only be sent to the agents you select. They never sell to a third party.

The Average Price of a Mobile Home in Major UT Cities,

- Salt Lake City: $54,567

- Provo: $38,858

- West Jordan: $62,143

- Orem: $41,617

- Sandy: $71,371

- Ogden: $25,066

- St. George: $59,827

What Is a Mobile Home Insurance Policy?

Mobile home insurance is a type of homeowners insurance policy that is tailored to the specific coverage needs and risks that owners of this type of home face. Mobile homes, also known as manufactured homes, have evolved over time and, since 1976, have been built to stricter HUD safety and building material standards. Manufactured homes are built in a factory and then transported to their final destination by truck. When they arrive at the site, they are secured to the ground with straps and anchors.

Despite the fact that these anchors are quite strong, homes without a below-ground foundation are more vulnerable to wind damage, especially in the event of a tornado. Modular homes, on the other hand, are constructed in sections in a factory before being assembled in their permanent locations. Because modular homes appreciate in value rather than depreciate and are permanently located, they are covered by standard homeowners insurance policies.

Average Home Insurance Utah

In Utah, the average cost of homeowners insurance for a $250,000 dwelling is $647 per year. This is less than the national average of $1,312 per year for homeowners insurance, and it is even less than the average premiums in neighboring states such as California and Colorado.

Related Articles: LANDLORD ATTORNEY: Tips for Hiring a Landlord-Tenant Lawyer

However, keep in mind that home insurance premiums vary depending on the age, size, location, and condition of your home, as well as the coverage options included in the policy. Furthermore, it is highly recommended that you shop around and request quotes from multiple insurance companies to ensure that you are getting the best rate for your home.

| State | The average annual cost of home insurance for $250,000 in dwelling coverage in neighboring states |

| Utah | $825 |

| Oregon | $776 |

| Colorado | $1,995 |

| Nevada | $814 |

| California | $1,101 |

Best Home Insurance Companies Utah

Purchasing a homeowners insurance policy from a reputable insurance company can mean the difference between getting your claim paid quickly after an accident and having to spend hours dealing with paperwork and red tape.

The complaint index from the National Association of Insurance Commissioners, the J.D. Power homeowners satisfaction survey, and the A.M. Best financial strength rating is three ways we judge the quality of homeowners insurance companies.

The NAIC complaint index compares the total amount of insurance sold by a company to the total number of complaints received. Also, a lower number indicates that there are fewer complaints, and the national average is 1.0.

Related Articles: FLOORING CONTRACTORS: Licence & Guide on How To Hire One

J.D. Power surveys are comprehensive evaluations of how satisfied homeowners are with their insurance companies. The scores range from 1 to 5, with 5 being the highest.

A.M. Best’s financial strength rating is a letter grade that describes how well-prepared a company is to withstand negative financial scenarios. This could include times when there is a high demand for claims (such as a widespread natural disaster) or a poor economic climate.

Common causes of loss in Utah

Most home insurers consider Utah to be a low-risk state, but there are still potential hazards to be aware of that could result in a property insurance claim. The following are the top recurring natural disasters in Utah, according to the Federal Emergency Management Agency’s (FEMA) record of declared disasters:

- Wildfires

- Earthquakes

- Storms in the winter

- Flooding

Fire and storm damage is covered by standard homeowner policies, but earthquakes and floods are not. Homeowners who live near an active fault line should consider buying separate earthquake insurance. If your home is in or near a flood zone, it may be worthwhile to investigate flood insurance. Also, if you have a mortgage on your home, your financial institution may require flood insurance.

Home insurance coverage options in Utah

Many insurance companies provide unique coverage options that competitors may not, but certain standard coverages are included in all homeowners insurance policies. To ensure you get the best homeowners insurance policy for your home, you should understand not only what these coverages are, but also how much insurance you’ll need for your home. Below is a brief summary of these coverage options:

Related Articles: Florida One Insurance: Home and Auto Insurance Reviews in Hialeah, Fl

- Dwelling coverage: This is the most important part of homeowners insurance because it protects your home and any attached structures.

- Other structures coverage: If you have a separate structure, such as a swimming pool or detached garage, this section of your homeowner’s insurance policy will cover it. The amount is typically a fixed percentage of the amount of your dwelling coverage.

- Personal property coverage: This insurance covers your personal belongings such as furniture, clothing, and appliances.

- Additional living expenses coverage: If your home was damaged as a result of a covered loss and you were unable to live there, this coverage would pay for temporary living expenses while your home was being repaired.

Frequently Asked Questions

How much is home insurance in Utah?

How much does home insurance cost in Utah? The average homeowner’s insurance policy costs $896 per year, or $75 per month. This is 48% less than the national average of $144 per month for home insurance.

Is homeowners insurance required in Utah?

For the 70% of Utah residents who own a home, homeowners insurance is critical financial protection.

Is home insurance and property insurance the same?

Although the terms “homeowners insurance” and “property insurance” are frequently used interchangeably, they are essentially the same.

Is home insurance really necessary?

You’re not required by law to have home insurance, but banks do require it as a condition of your mortgage. Homeowners’ insurance can assist you in protecting yourself from massive financial loss. It can also help cover the cost of compensating others for bodily harm or property damage.

What is not covered by homeowners insurance?

Damage from termites and insects, birds or rodents, rust, rot, mold, and general wear and tear are not covered. Smog or smoke from industrial or agricultural operations is also not covered. If something is poorly constructed or has a hidden flaw, it is generally excluded and will not be covered.